Reduce Debts with a DSA

A DSA (Debt Settlement Arrangement) is a debt solution designed to help people that are having difficulty repaying debts. A DSA could:

lower payments to an affordable amount.

offer formal protection from lenders.

freeze all interest & charges.

write off unpaid debts on completion.

Fill in the form to find out more. We will assess your situation and advise if a DSA is an option for you. We offer free, confidential, no obligation advice. * A DSA is not a loan.

Find out if you qualify

How does it work?

Firstly, you have a chat with one of our advisors to see if it is your best option. We analyse your financial situation and work out what you can realistically afford to pay to your creditors, after giving priority to your other expenses. With the help of our PIP's (Personal Insolvency Practitioners) we can negotiate with your creditors and take you through the process of a DSA from start to finsh.

When a DSA is agreed, it becomes legally binding for you and your creditors. You can then start your lower repayments. After 60 months (usual term of a DSA), you are free of your debts and any remaining unpaid debt is written off.

The need to knows

-

Who can do a DSA?

Almost anyone can do a DSA. You can be single, married, employed, self-employed, a homeowner or a tenant...

There are certain criteria in order to do a DSA, such as debt level and number of creditors, but we can discuss this further when we chat. If a DSA is not suitable, we can recommend other various options for you to consider.

-

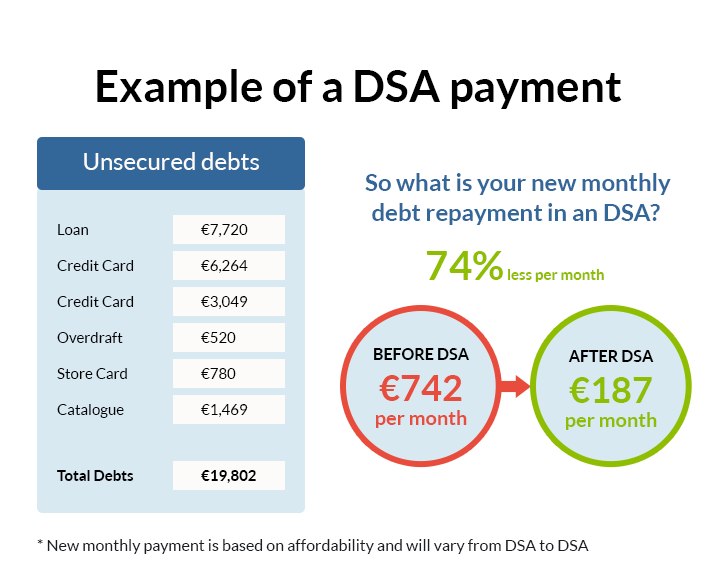

How is my DSA payment calculated?

Your DSA payment is calculated by analysing your income and expenses on a monthly basis (not including any debt repayments). We then work out how much money you have left over each month. This left over amount is your potential DSA payment.

-

How much does it cost to do a DSA?

We do not charge for our advice and we do not charge upfront fees as we believe this to be unethical. You will never receive a bill from us.

Only if your DSA is accepted will we receive any payments for fees. If your DSA is not accepted then you pay nothing. Our fees vary depending on your circumstances and they are built into your monthly payment to your creditors which will be explained in your proposal. It is your creditors who determine what we get paid and we cannot draw fees without their approval.

Why choose National Debt Relief?

1) No upfront fees or consultation fees - Saving you time and money

We are one of the only DSA companies who do not charge upfront fees. Paying any provider upfront fees will only cause a delay in your DSA being accepted and cost you extra money that is completely unnecessary. If your DSA is rejected you will lose this money. DO NOT PAY UPFRONT FEES EVER!

2) High acceptance rate

We have an amazing acceptance rate for DSAs proposed. We know any DSAs we propose will have a great chance of being accepted. We also fight very hard for every client to make sure their DSA proposal is carefully considered by the creditors. Our proposals will always be based on something that is affordable and because of this every DSA we propose will be unique.

3) Excellent Customer Service

We have an excellent customer care team. We are a family run company and our advisors have all been with us for many years. They are highly trained and will be able to answer any question quickly and professionally. You will also find us very friendly.

5) Reputation and Experience

Our company is part of McCambridge Duffy, a company that has been established for 80+ years. In this time we have gained a reputation for our ethical approach. We only recommend a DSA if it is your most appropriate option, and all other options will be discussed too. We are one of the best known Insolvency companies in Ireland and have already successfully helped many people deal with their debts.

Our Philosophy

At National Debt Relief we are driven by providing just that...

"Debt Relief" to people who really need it.

We believe that everyone should have access to sound advice, information and the best possible options for their situation. We pride ourselves on offering good quality, caring customer service.

Our philosophy is reflected in the feedback we receive from our many happy clients and the results in the successful plans we put forward. Read some of our testimonials below taken from our many client reviews.

Client Testimonials

-

Very friendly reassuring confident personal service

Very reassuring staff whom handled my situation very professionally and made me feel very confident that I had the support I needed from start to finish. Always keeping me up to date and advising me of my options. Their service was seamless and the conclusion was as I hoped.

If you are in need of advice just call them. If its possible they will help you too.

-

General Debt Advice

We offer a free advice only service where we can review your financial situation and let you know of all of your options.

-

PIA

We also offer PIAs; a Debt Solution that can help you deal with mortgage difficulties and other debts.

-

Bankruptcy Advice

If Bankruptcy is your only option, we also offer Bankruptcy Advice.

Who can do a DSA?

A DSA can be used by nearly all Irish residents.

- Single people where debt is in just one persons' name

- Married / Co-habiting people where debt is in joint and single names

- Business Owners and Self Employed people

- Homeowners with one house or many

- Tenants

It really is suitable for lots of different situations.

What are the living costs in a DSA?

Anything you need to pay regularly is classed as a living cost. For example, Mortgage/Rent, Food/Groceries, Clothes, Travel/Transport, Car HP, Fuel, Parking costs, Council Tax, Electricity, Gas, Heat and Light, Phone, Mobile, Internet, even Sky TV if you have it...

In a DSA you will have an agreed budget for your all your living costs. These expenses will be mostly based on what you currently have to pay out each month. You should declare all normal monthly expenses so we and your creditors can understand the full extent of your situation. There may be restrictions on some expenditure items, such as mobile phone for example. There may also be extra allowance for special circumstances in some cases.

How do I go about setting up my DSA?

Initially all you need to do is simply fill in the form. By doing so you are asking us to review your current circumstances and advise whether a DSA is indeed the most appropriate solution to your problems.

If a DSA is deemed appropriate, and you still wish to pursue this option, we provide you with an opportunity to ask one of our specialists any further questions you may have. We will then produce your Prescribed Financial Statement (PFS) application, which is sent to the Insolvency Service of Ireland (ISI) and the Court.The court then grants your Protective Certificate (offering you legal protection from your creditors). Our PIP will then draft your DSA proposal for your creditors to vote on. Atleast 65% (by debt value) must vote in favour of your proposal.

The ISI, Court and your creditors carry out a final review, before approving your DSA. Once it is approved, it becomes legally binding and your DSA payments can begin. We will assign dedicated case managers to look after your DSA for it's duration. When your DSA is complete, you will be discharged from your debts. Any outstanding balances will be cleared and you can start over debt free.

Will my credit rating be affected in a DSA?

Your credit rating will be affected in a DSA (if it has not already been affected anyway). However, according to Credit Reference Agency Stubbs Gazette, once you are in the DSA and have successfully kept up with payments for more than 24 months, your credit rating will begin to repair itself. When you have completed your DSA, your credit score will have been rehabilitated entirely. See Quote below

" We have recently reengineered our own consumer credit scores...so if a debtor enters into a Personal Insolvency Agreement or a Debt Settlement Arrangement and makes all of their payments on time, after 24 months their credit score will begin to repair. Their score will continue to improve over the next 3 to 4 years until at the very end of the arrangement their credit score will have been rehabilitated entirely. "

James Treacy, CEO Stubbs Gazette

DSA Advantages

- You only have to make one affordable monthly payment or in some cases a one-off payment

- Your monthly payment will be affordable and within your monthly budget.

- We do not charge any upfront fees or consultation fees, saving you €100's and also allowing for a faster set-up time.

- The stigma of bankruptcy is avoided

- A DSA offers you and your assets legal protection from your unsecured creditors.

- Unsecured debts cleared within 60 months

- A DSA can be complete in as little as 1 year if you can offer a lump sum payment

- All interest and charges are legally frozen.

- An DSA is suitable for homeowners, indivduals or couples and even business owners

DSA Disadvantages

- Your credit rating will be affected and you cannot obtain further crediter whilst in the DSA.

- If your circumstances change, and your PIP can’t get creditors to accept amended terms, the DSA is likely to fail.

- If you fail to make payments on time or fall into arrears your DSA could fail.

- Your DSA will be entered onto a public register.

How long does a DSA last?

Typically a DSA can last for about five years, but in some cases this can be extended. It is also possible to do a DSA in a shorter period of time, if you can produce a partial or full lump sum of money. The good thing about a DSA agreement is you will know exactly when it is complete as it will be outlined in your agreement.

Will my creditors agree to a DSA?

Most creditors are fully aware of a DSA, as it's been in existence for a number of years now. If 65% of your creditors by value vote in favour of your DSA, then all creditors are bound by its terms. Creditors can suggest alterations to your proposal and you can choose whether to accept them or not. If your creditors vote against your proposal, then there is an appeals process or you still have the option of an informal arrangement.